Happy belated March data.

A lot happened in March 2020. The stock market dropped 30% seemingly overnight, hospitals were overwhelmed with COVID patients, entire cities shut down, and social distancing became a thing. Regarding metro Detroit real estate and beyond, the data tells the story.

Key Takeaways:

- Metro Detroit March activity down, median prices up

- March new home data worse than expectations

- Interest rate trends heading south, may go sub 3% in 2021

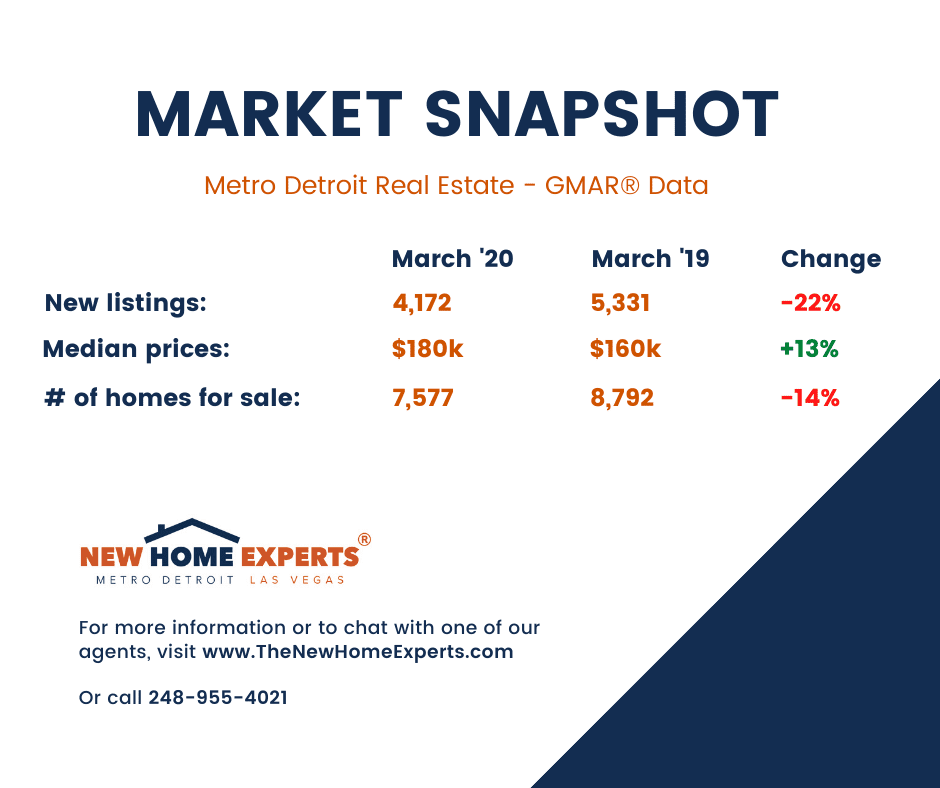

March in Metro Detroit

Heading into March, both agents and buyers were getting giddy for the beginning of the spring selling season. Locally, we saw a number of new (and used) homes hit the market and were excited for more to come. It was one of the few times in the year we could match more than 5 (or so) properties with one of our many buyers waiting in the wings because inventory is in the tank.

Then, Corona started to become reality.

We saw listings that would otherwise sell quickly sit a bit longer and some listings even withdrawn. On the flip, as bad as things became with the lockdown around mid-March, we still saw homes going pending within days. Everyone seemed to be confused and most decided to wait, which is where we still stand in early April regardless of heroic efforts to show homes virtually.

At the end of the day, March was challenging and changed our outlook on the Spring market. We did experience some closing successes regardless of the pandemic, and overall as expected sales activity like new listings and the number of homes for sale decreased. The good news? Median prices were up double digits: 13%.

National New Home Data

Homebuilding had it’s worst month (March) since 1984. Specifically, housing starts were down 22% from the previous month (vs. a 15% decrease expected). Also, sales were down 9% from a year ago. Surprised? Humans couldn’t go near each other. They couldn’t visit models. Trades couldn’t build. Everything just stopped.

The good? Prior to the outbreak sales for the quarter were actually up 6.7% vs a year ago. Plus, the median new home sales price for March was $321,400, up from $310,600 a year ago. All positive data for the industry.

Locally, builders we spoke with experienced little to no new activity, canceled sales, and pushed to encourage virtual tours. In the midwest, sales dropped 8.1%, the second smallest drop in the nation. Heading into this mess the fundamentals were solid; low inventory competition from resale, stable (even rising) prices, super low interest rates, and the Spring selling seasonality.

Even though both local and national builders made a quick pivot to virtual tours and 100% online sales, the fear about what’s to come kept almost all buyers on the sidelines.

Theres hope, though, this can be quick if we abide by the rules and do the right thing by staying apart. If we do so we can likely return to expectations sooner rather than later. We’ll just push Spring selling activity forward a couple months. Plus, interest rates are heading south!

Interest Rate Trends

Despite all this…mortgage rates remain low. From March 5 we saw a low in the 30 year fixed of 3.29% to a high on March 19 of 3.65%; all ridiculously low rates considering where we find ourselves. See Freddie Macs chart here for weekly data.

Regardless of where rates are at today, we’re likely in for a wild ride over the next 12-18 months, according to this Realtor Magazine article. In fact, economists at Fannie Mae’s Housing Forecast report are predicting the average 30 year fixed for 2020 will drop to 3%, then into the mid 2% range into 2021! Rates like that on a 30 year fixed mortgage would be unprecedented, and present more buying and approval power for buyers in the market.

Despite expected rate drops, and despite the COVID pandemic, economists at Fannie Mae expect prices to increase about 2.5% into 2021. A perfect formula for buyers getting into the market.

{kind=link}

More Articles

Metro Detroit

THE NAR SETTLEMENT

Real estate is back in the news and as you might’ve heard, um, some things have happened. Primarily, the NAR...

April 15, 2024

Read More

Metro Detroit

NEWSLETTER: APRIL 2024

NAR YOU SERIOUS OUR THOUGHTS ON THE (POTENTIAL) SETTLEMENT Last Month the National Association of Realtors (NAR) settled the commission's...

April 14, 2024

Read More

Metro Detroit

1933 CAMROSE COURT

New construction that is move-in ready, 1933 Camrose Court features a spectacular new custom ranch home by Strathdale Development. Nestled...